In air transport, India can be considered as an Eldorado. Yet, very few Indian airlines derive financial benefit. Let's try to analyze why, by shedding light on this market.

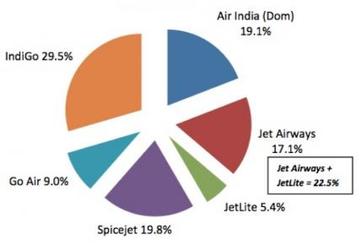

Six major airlines are operating in India. Their respective market shares are the following:

• Air India 19.1%

• Go Air 9.0%

• Indigo 29.5%

• Jet Airways 17.1%

• Jet Lite 5.1%

• SpiceJet 19.8%

Source : Directorate General of Civil Aviation - May 2013

Air India, state-owned airline, accused a US$ 1.4 billion deficit at the end of 2012 and must be supported regularly by the central state. Jet Airways ( Jet Airways +Jet Lite) group has hardly been a profitable for the last 5 years. At the end of 2012, it had a deficit of US$ 250 million to an income of about US$ 3 billion. SpiceJet was in deficit of US$ 109 million for a turnover of 720 million US$ in 2012. Following the recent departure of its CEO , SpiceJet has the opportunity to renew its management team and restore confidence. Go Air has lost US$ 24 million for US$ 278 million sales in 2012. Go Air is still in deficit but approaches equilibrium. Indigo seems healthier than its competitors, with a profit of US$ 23 million for an income of US$ 1 billion in 2012.

How to explain the relative success of Indigo ?

The fill rate at Indigo is more than 80 % while it is between 65% and 75% for other airlines. The "pitch" (the difference between two rows of seats ) is 76 cm in Indigo Airbus A320 when it goes up to 81cm on Air India or Jet Airways B737 A320 . More seats in tight rows , and especially a better fill rate than its competitors thus explain the relative success of Indigo .

"Low Cost" a Key Success Factor in India?

Indeed , Indian specificity 2/ 3 of the market in the hands of " Low Cost Carriers" ( Indigo , Jet Airways , Go Air, SpiceJet ). Only Air India and Jet Airways are still operating as "Full Service Carriers". One the most significant event of the year 2013, was the bankruptcy of Kingfisher, a full service airline. It underlined the fragility of the sector. The airline , however, was the largest in the country less than two years earlier and had an excellent reputation among passengers . Kingfisher 's bankruptcy underscores the appetite of the Indian consumer ( including passengers ) towards low prices. The average annual per capita GDP is just over 1000 Euro . Each rupee is valuable ... In this country of 1.3 billion people , there are only 60 million domestic passengers in 2012. The vast majority of the population have therefore never flew .

Other factors impacting air transport market ?

Actually, this market is highly regulated by the government. The price of kerosene is burden by more severe taxes than in other countries. Airport infrastructure are still largely in the making, although efforts have been made in the last five years ( including Delhi). Faced with the difficulties of the actors and a promising market , the Indian government decided in September 2012 to review the law on foreign direct investment (FDI : Foreign Direct Investment). The government now allows foreign investors to own up to 49% of the share capital of Indian airlines. The change in legislation has opened the ball of contenders ...

TaTa Sons will soon be present in the capital of two new entrants. First Air Asia India, low-cost company and also a joint venture with Singapore Airlines that will provide a comprehensive and high quality service. Some may see it as a contradiction. Tata not see any. Both offers are aimed at very different segments of the market. Analysts are questionning the viability of the project of alliance between TaTa Sons and Singapore Airlines in launching an airline rather " premium". While the low-cost airline Air Asia India, might be gain a large market share. However, the Indian group TaTa already sees opportunities to streamline aircraft maintenance.

Translated from French by Frederic Gayraud, PRADO CONSULTING

Published on Le Cercle Les Echos

Six major airlines are operating in India. Their respective market shares are the following:

• Air India 19.1%

• Go Air 9.0%

• Indigo 29.5%

• Jet Airways 17.1%

• Jet Lite 5.1%

• SpiceJet 19.8%

Source : Directorate General of Civil Aviation - May 2013

Air India, state-owned airline, accused a US$ 1.4 billion deficit at the end of 2012 and must be supported regularly by the central state. Jet Airways ( Jet Airways +Jet Lite) group has hardly been a profitable for the last 5 years. At the end of 2012, it had a deficit of US$ 250 million to an income of about US$ 3 billion. SpiceJet was in deficit of US$ 109 million for a turnover of 720 million US$ in 2012. Following the recent departure of its CEO , SpiceJet has the opportunity to renew its management team and restore confidence. Go Air has lost US$ 24 million for US$ 278 million sales in 2012. Go Air is still in deficit but approaches equilibrium. Indigo seems healthier than its competitors, with a profit of US$ 23 million for an income of US$ 1 billion in 2012.

How to explain the relative success of Indigo ?

The fill rate at Indigo is more than 80 % while it is between 65% and 75% for other airlines. The "pitch" (the difference between two rows of seats ) is 76 cm in Indigo Airbus A320 when it goes up to 81cm on Air India or Jet Airways B737 A320 . More seats in tight rows , and especially a better fill rate than its competitors thus explain the relative success of Indigo .

"Low Cost" a Key Success Factor in India?

Indeed , Indian specificity 2/ 3 of the market in the hands of " Low Cost Carriers" ( Indigo , Jet Airways , Go Air, SpiceJet ). Only Air India and Jet Airways are still operating as "Full Service Carriers". One the most significant event of the year 2013, was the bankruptcy of Kingfisher, a full service airline. It underlined the fragility of the sector. The airline , however, was the largest in the country less than two years earlier and had an excellent reputation among passengers . Kingfisher 's bankruptcy underscores the appetite of the Indian consumer ( including passengers ) towards low prices. The average annual per capita GDP is just over 1000 Euro . Each rupee is valuable ... In this country of 1.3 billion people , there are only 60 million domestic passengers in 2012. The vast majority of the population have therefore never flew .

Other factors impacting air transport market ?

Actually, this market is highly regulated by the government. The price of kerosene is burden by more severe taxes than in other countries. Airport infrastructure are still largely in the making, although efforts have been made in the last five years ( including Delhi). Faced with the difficulties of the actors and a promising market , the Indian government decided in September 2012 to review the law on foreign direct investment (FDI : Foreign Direct Investment). The government now allows foreign investors to own up to 49% of the share capital of Indian airlines. The change in legislation has opened the ball of contenders ...

TaTa Sons will soon be present in the capital of two new entrants. First Air Asia India, low-cost company and also a joint venture with Singapore Airlines that will provide a comprehensive and high quality service. Some may see it as a contradiction. Tata not see any. Both offers are aimed at very different segments of the market. Analysts are questionning the viability of the project of alliance between TaTa Sons and Singapore Airlines in launching an airline rather " premium". While the low-cost airline Air Asia India, might be gain a large market share. However, the Indian group TaTa already sees opportunities to streamline aircraft maintenance.

Translated from French by Frederic Gayraud, PRADO CONSULTING

Published on Le Cercle Les Echos

RSS Feed

RSS Feed